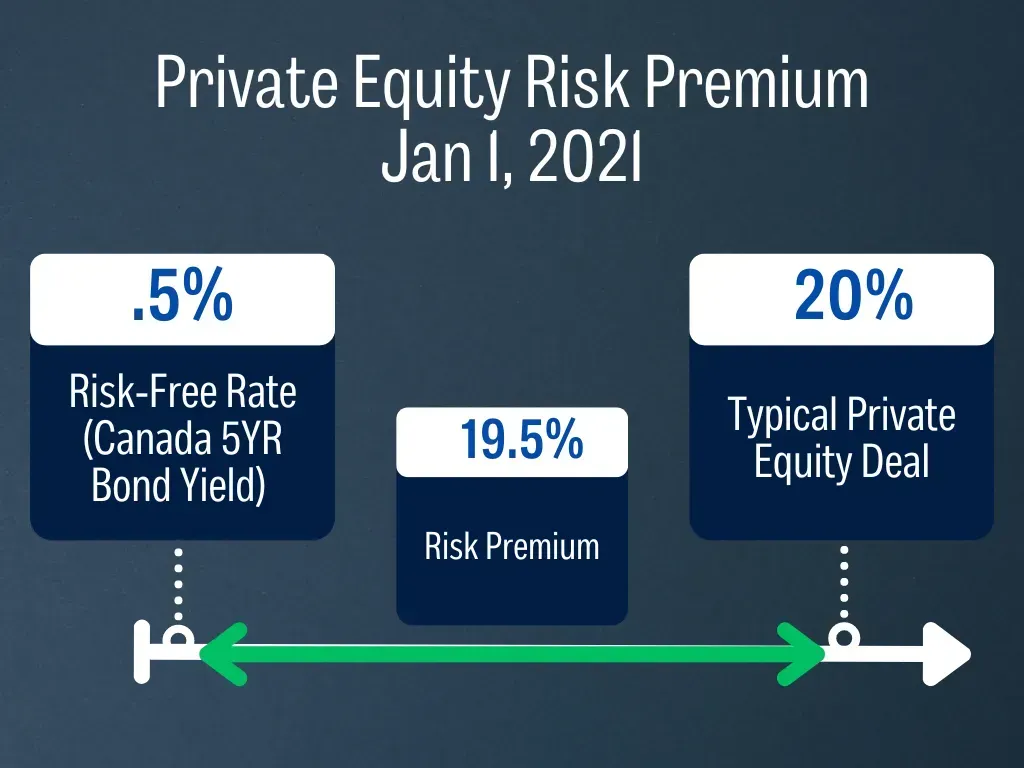

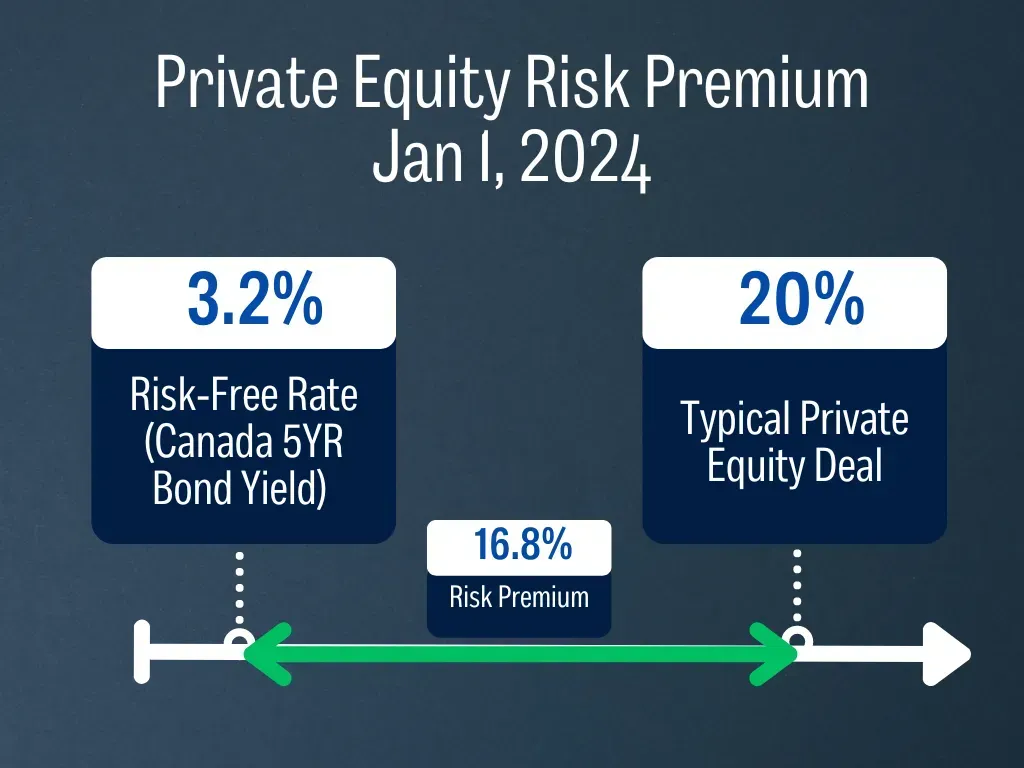

Off the top, note how the higher risk-free rate in 2024 cuts into the risk premium, meaning that even if deals are projecting similar returns, they are less attractive on a risk adjusted basis.

Second, and more interestingly, on the deals we have seen, projected deal returns between 2021 and 2024 haven’t changed much. Here’s why that’s problematic in many situations.

Most development deals rely on debt to some extent, and with higher interest rates, the costs of carrying that debt has increased, which pushes down returns.

To make up for this, we’ve found that a growing number of developers have used more aggressive assumptions in their underwriting to project similar levels of returns, such as projecting high rent growth, lower levels of vacancy, faster lease-up, future interest rate decreases, etc.

Reality may unfold in line with these more aggressive assumptions, though there is a lower probability of this happening.

In short, in the current environment the risk premium on development deals is lower, and in our view, the risk of not meeting projected returns is higher.

There are still excellent developers doing exciting deals, though to be attractive in this market, these deals have to be substantially de-risked, use conservative assumptions in underwriting, and present above average return potential.

With that framework set, let’s look at the areas where we think opportunities for superior risk-adjusted returns are most likely in 2024.

Areas of Opportunity

Mortgage Funds

We think that mortgage funds will continue to offer excellent risk-adjusted returns in 2024. When you can get equity-sized returns with debt-level stability and defensive positioning, investing in debt is something worth considering.

If you look at the TSX Composite Index, over the 50 year period from November 30, 1971 to November 20, 2021 the average annualized return was 7.94%. Debt products are delivering returns in this realm, if not higher. One of our fund partners delivered over 10% returns (net of fees) last year and is projecting similar returns this year.

Compared to the 2 year bond rate at ~4%, we think that the returns from our partner funds are highly attractive relative to the associated level of risk.

Select US Multi-family

Out of all of the asset classes we’ve invested in over the past 5+ years, US multi-family properties have been one of the hardest hit. There are many contributing factors, including rising interest rates, higher renovation costs, and substantially higher operational costs, particularly insurance and property taxes.

New residential developments that started two or three years ago during the strong market are now coming online, leading to increased vacancy and decreasing rental rates. Lenders are also more hesitant to lend in this environment, offering lower loan to values and more restrictive loan terms. The result? Many multi-family properties in traditional growth markets are down over 30% from peak pricing.

Identifying the bottom of the market is a difficult task, though we believe that in a world where high-quality assets are selling below replacement cost, there are likely to be some unique opportunities with an attractive risk-adjusted return.

One potential strategy may be to purchase these multi-family properties using very little debt, waiting for the market to improve, and then refinancing the property to return investor equity and increase returns. This would give investors the staying power to ride out any market turbulence over the next few years.

Special Situation Residential Development Deals

We are beginning to see another compelling category of deals; Canadian residential developments that started two or three years ago that need more cash to complete, usually due to higher than anticipated construction and interest costs. Many of them still look to be quite profitable as projected revenues have increased as well.

These types of deals have multiple benefits. Many of them have little to no entitlement risk as they are fully rezoned and have already received (or are about to receive) development and building permits. In a number of markets that we work in, particularly in BC and Ontario which are notorious for slow moving development processes, being able to remove development risk is a big advantage.

The second benefit is having much more clarity on costs and projected revenues, as we have the added benefit of additional information that the developer did not have at the time of purchase.

The last potential benefit is higher annualized returns due to having a shorter time-horizon than the original investors.

It all adds up to lower risk and potentially higher returns and we hope to see more of these “special situation” deals in 2024.

Conclusion

We are optimistic for a better environment for deals in 2024, particularly in the latter half of the year if interest rates start to come down. The quality of the deals that we are seeing has definitely increased over the last few months, maybe not to the point where we are proceeding, but some have been attractive enough to get a second or third look. This wasn’t the case for most of the deals we were seeing for most of 2023.

As always, we are here to bring you the best deals possible, and are prepared to hold off on doing equity deals entirely until we see an opportunity that meets our underwriting standards.

In the meantime we continue to believe that in this high-rate environment, investing in debt is a great option.