What we like

There’s lots to like about investing in multiplex housing, so let’s start with the strong points:

- You can buy the land needed quickly and (relatively) inexpensively.

When compared to the land assembly process, which is usually necessary to support multi-family projects in developed areas, it is easier and less expensive to buy a handful of single family lots in good locations.

- Shorter permitting and construction times

Comparatively, these are simpler projects, which leads to shorter development and building permit processes, as well as construction timelines.

- Shorter project timelines provide for (slightly) more visibility into the future

We aren’t advocates of using the crystal ball around here, though when project timelines are less than 2 years, and sales begin even earlier, it makes it easier to establish reasonable assumptions for both costs and revenue based on the current environment.

Not needing to provide underground parking and less common space reduces overall building costs.

Shorter timelines make for attractive IRRs. The challenge is that returns are highly sensitive to any delays or slow market conditions for unit sales.

What could go wrong

There are diverse ways that things can go wrong with any real estate project, and even though this strategy is comparatively simple, investors should be aware of potential pain points that are unique to this strategy:

One of the pros of this strategy, effective utilization of the whole property for building space, does have obvious drawbacks with limited or no parking and minimal outdoor space. Even if the purchase prices are lower than options with these amenities, proximity to transit and parks becomes more important.

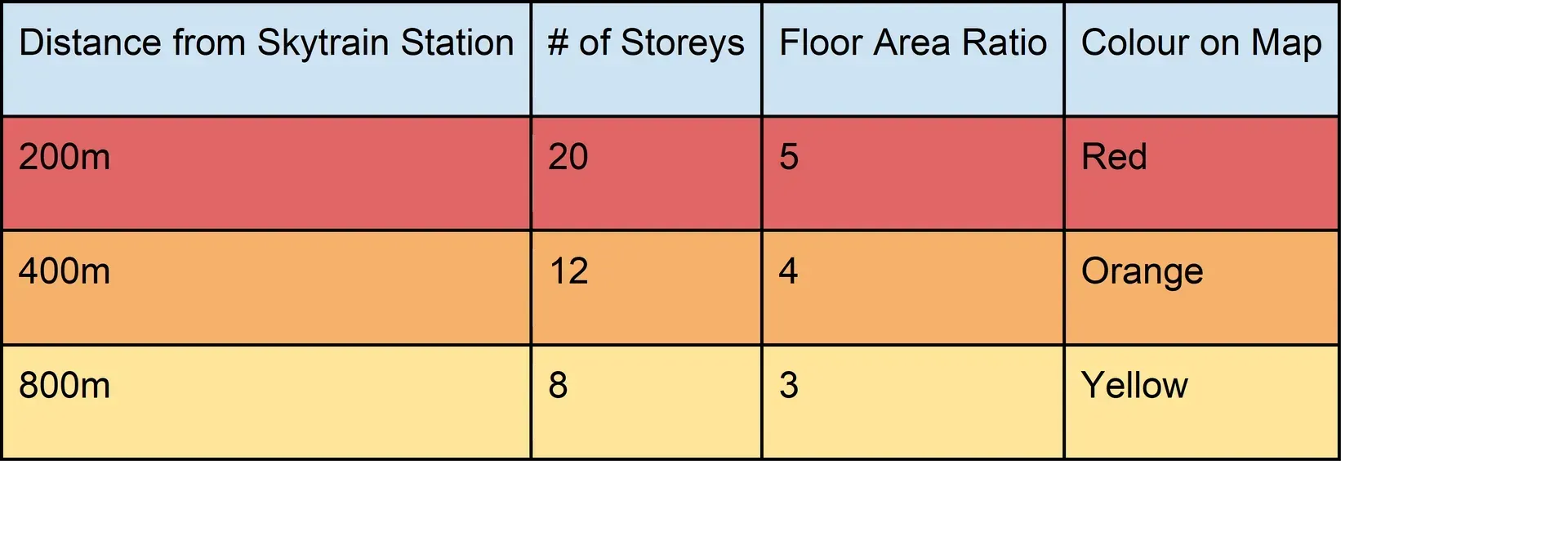

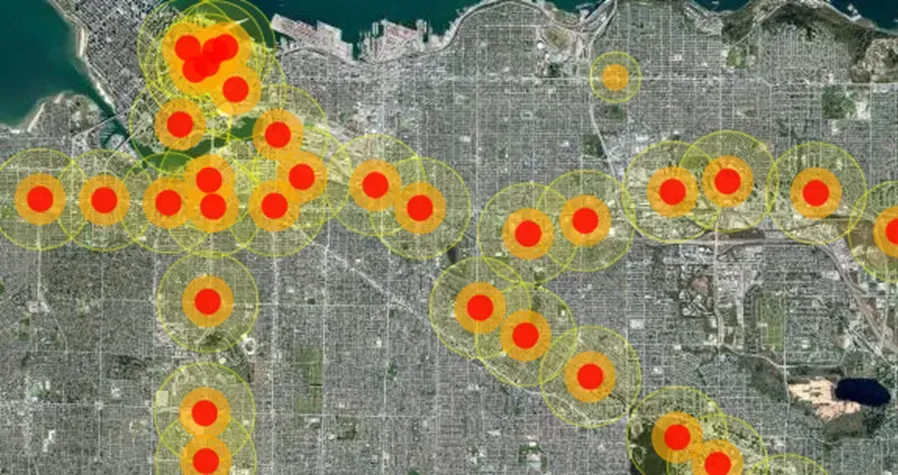

Unfortunately, we suspect that most multiplexes will be built outside of Transit Oriented Development Areas (otherwise, why wouldn’t they be developed to even higher density), so it can put these projects in a bit of an awkward spot for transportation.

To date, multiplexes have been hoovered up by purchasers, but it remains to be seen how deep the buyer pool is for this style of property compared to more traditional styles such as condos, townhomes, and duplexes. The level of demand is one reason we suspect this is a strategy where it will be better to be early than late. Another is that each additional multiplex on a street may exacerbate parking issues, which may make the 10th multiplex on a street a less attractive product than the 1st multiplex on a street.

One major challenge with this type of development is that infrastructure in single family neighbourhoods is often insufficient to support anything more than single family houses. Sewer pipes could be undersized and electrical upgrades may be required, etc. In our experience and from conversations with developers, negotiating who pays for what upgrades and setting up latecomer agreements can present both a time and financial hurdle with this type of development.

- Finding the Right Development Partner

Finding the right development partner is always critical, and the size and scale of these projects generally lends itself to small to mid-size developers, where the track record may not be as extensive, or there is less capacity to implement this strategy at scale.

Conclusion

At Hawkeye, we pride ourselves on being strategy agnostic. We are regularly out looking for the strategies and jurisdictions that present the most attractive real estate investment opportunities. What this means is that we get to look under a lot of hoods.

For the most part, we like a lot of what we see with the BC multiplex strategy and there is likely opportunity here for investors. While we haven’t found the right project to take a swing at this strategy just yet, we are keeping our eyes and ears open.