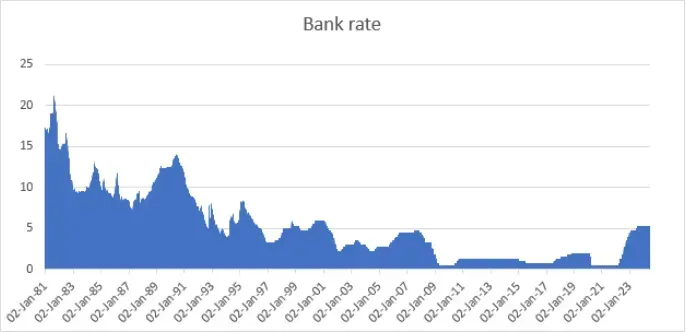

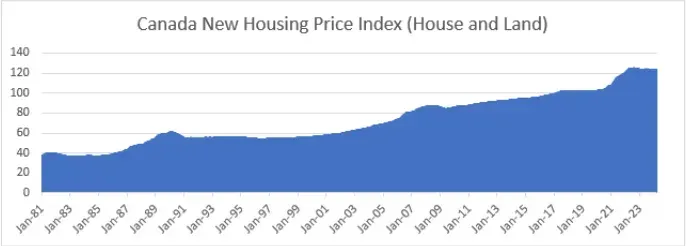

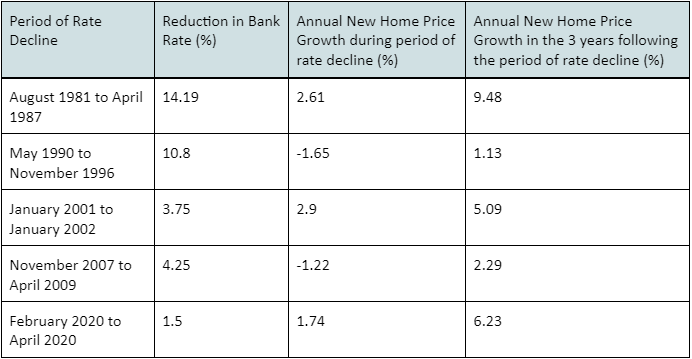

Each of these periods saw wildly different economic circumstances, and interest rate is only one variable in what causes changes in home price, but for the purposes of this article, it suffices to point out there has historically been a trend of below average price growth in periods of falling rates, followed by a period of above average appreciation.

The average annual new home price growth during the combined 14.83 years of rate decline considered above was 0.38%.

Why? In general, the Central Bank lowers interest rates in response to economic weakness. The low or negative GDP growth, higher unemployment and slower wage growth during these periods tends to slow home price growth more than the added affordability that comes with lower borrowing costs.

However, in the 3 years that follow a period of rate reduction, real estate has historically performed well. The average annual new home price growth during the combined 15 years following periods of rate decline was 4.84%, as lower borrowing costs along with an improving economy supported high price growth.

It’s also worth noting that in addition to the differing economic circumstances from today, these periods saw much larger rate decreases than we are likely to see in 2024-2025, so it’s difficult to know how applicable these previous scenarios are for forecasting.

Conclusion

This has been a whole lot of writing to come to some rather simple conclusions.

First, preparing yourself to be successful in any rate environment is much more fruitful than trying to predict where rates are going.

Second, when you see social media gurus, journalists, or industry insiders asserting that rate cuts are going to cause real estate prices to suddenly increase (Bank of Canada interest rate cut could be ‘tailwind’ for GTA real estate), know that they might be right, but that historically, price growth has been slower during rate decreases.

Third, owning real estate during periods of rate decline hasn’t been particularly rewarding, but the years following have been exceptional.

We don’t know how much and how fast rates will fall, how resilient our economy will be, or who will form government in the next election.

But that uncertainty is causing plenty of fear in the market, and frankly, we don’t mind that. It’s not the time to be swinging at every opportunity, but for those keeping their ear to the ground, there are genuinely exciting investment opportunities in this market.